Warnings about a shortage of credits under the future aviation carbon market are unfounded. The upcoming decision on what airlines will be able to buy must, therefore, focus on ensuring that only credits from high-quality projects are eligible.

It is crunch time again for the ICAO Council, the UN aviation agency’s decision-making body comprised of 36 member states from around the world and tasked with setting out rules for international civil aviation. At its upcoming meeting in March, it is expected to decide which offsets airlines are allowed to use to meet their objective of so-called “carbon-neutral growth” from 2021 under CORSIA, the aviation sector’s carbon market

These discussions echo the negotiations on the future of carbon markets taking place under the Paris agreement, and which collapsed for the second year in a row last December. However, it is much more likely that countries will come to an agreement at ICAO because the decision does not require unanimity among all UN countries – as is the case at the UNFCCC – and the time pressure is high to ensure that CORSIA can enter into operation from 2021.

In this context, some countries and representatives from aviation and carbon market industries are trying to promote the use of old, junk offsets which would be extremely cheap for airlines to purchase, and would do nothing to solve the climate crisis, e.g. credits from the UN’s Clean Development Mechanism (CDM). The main argument has been that the large demand for offsets by airlines will create a shortage of units on the market, and will make it impossible for airlines to meet their climate targets.

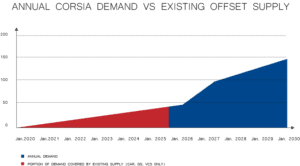

This is nothing but scaremongering. In fact, the opposite is a much more realistic threat, as a flood of cheap credits could enter the aviation sector’s carbon market if restrictions are not stringent enough. Some estimates have put the potential supply of credits upwards of 15 billion, while demand is expected to be in the range of 1.6 to 3.7 billion. While these represent potential supply estimates, i.e. the number of credits which could enter the market if projects decided to continue their operations and sell credits for their emission reductions, the existing supply would also be enough to meet CORSIA demand for years.

For instance, we analysed the availability of offset credits which airlines could purchase today if the three main voluntary market programs were found to be eligible under CORSIA. The result is that this supply would be sufficient to cover demand from airlines well into 2025. This would leave plenty of time for new projects to develop.

On a more fundamental level, promoting the use of low-quality offsets under CORSIA for the sake of ensuring market liquidity demonstrates a clear lack of understanding of both the severity of the climate crisis and the functioning of carbon markets.

In a world where we continue to emit approximately 37 billion tonnes of CO2e every year, it is hard to imagine there will not be enough opportunities to generate emission reductions and supply airlines with carbon credits. The real concern is not the supply. The real concern is the price. The average price of an offset credit in 2019 was 3.01$. If the supply of credits truly was to decrease significantly, the prices would rise, and developers would run to implement new projects. There is no shortage of ideas to cut emissions, only a shortage of money.

Decisionmakers at ICAO will, therefore, have to look past the scaremongering and take the necessary measures to ensure that only high-quality offsets, issued by projects started in 2020 or later, will be eligible for use under CORSIA.