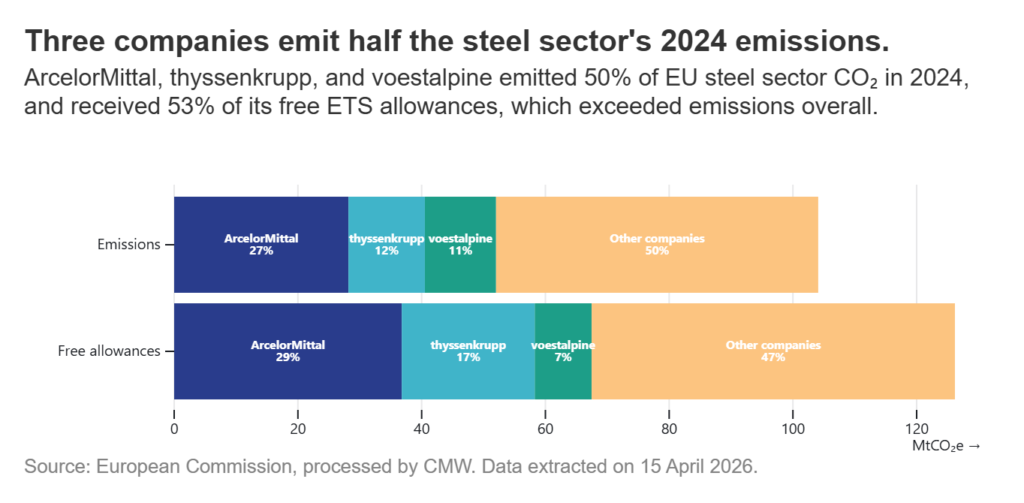

The deep divide in the steel lobby shown through numbers

On 15 June 2026 a group of companies – including major European steelmakers ArcelorMittal, thyssenkrupp, voestalpine – addressed a letter to the European Council calling for “immediate action to halt the escalation of ETS-related costs and avoid further damage to Europe’s manufacturing base.” The letter was strategically timed, sent in the leadup to the European Commission’s review of the EU Emission Trading System (EU ETS), due to launch on the 17th of July.

A few weeks later, a second letter landed in the Berlaymont inbox, this time sent by steelmaking competitors including SSAB, Salzgitter and Outokumpu. That letter demanded more or less the complete opposite of letter one: calling on policymakers to stay the course with the ETS, decrease emissions in line with the 2040 targets, and maintain the trajectory of phasing out the free allocation of emission allowances – the currency of the ETS.

It is intriguing that powerful companies representing the same industry hold polar opposite views on how the forthcoming revision should play out. However, recent financial decisions taken by ArcelorMittal, thyssenkrupp and voestalpine to prolong the lifespan of their coal-based plants indicate what may be the motivating factor.

A profitable loophole

Steelmakers have historically been able to gain from the EU ETS. Years of receiving a surplus of free pollution permits – above their actual emissions output – has led to several companies enjoying windfall profits. What’s more, these same companies are passing down a substantial share of these windfall carbon costs incurred, for emissions they didn’t even have to pay for, directly down to their consumers. Research shows that firms with the most market power are those who bagged the highest over-allocation profits.

The picture becomes even clearer once you consider that these same companies receive public funding from compensation schemes that cover the carbon costs of their electricity usage, as well as a top up from the state aid budget to support their announced (and in some cases cancelled) decarbonisation projects. The EU ETS is anything but a burden for some steel companies.

Meanwhile, the EU carbon market is finally set to start applying some pressure on polluting industries, including steelmakers. Carbon prices are slowly increasing over time, and the Carbon Border Adjustment Mechanism is now enabling free allocation of allowances to be gradually reduced.

Production of iron and steel is responsible for 7% of total emissions under the EU ETS: processes and technologies must evolve rapidly to keep pace with the necessary decarbonisation pathway. One of the most significant polluting assets in the steelmaking process are coal-based blast-furnaces (BF), the technology used most commonly to produce primary steel. The so-called BF-BOF route (blast furnace – basic oxygen furnace) generates a colossal 2.3 up to 3 tonnes of CO2 per ton of steel.

The forthcoming ETS revision must lay the groundwork to phase out these plants entirely and replace them with lower emitting technologies, such as electric arc furnaces (EAF) and direct reduced iron (DRI) plants powered by renewable energy and green hydrogen. These technologies are proven to reduce emissions – are readily available – and in the case of EAF are commercially scaled in other jurisdictions. So are European steelmakers investing in this decarbonisation path? If not, how are they investing their profits? And what role does the EU ETS play in these choices?

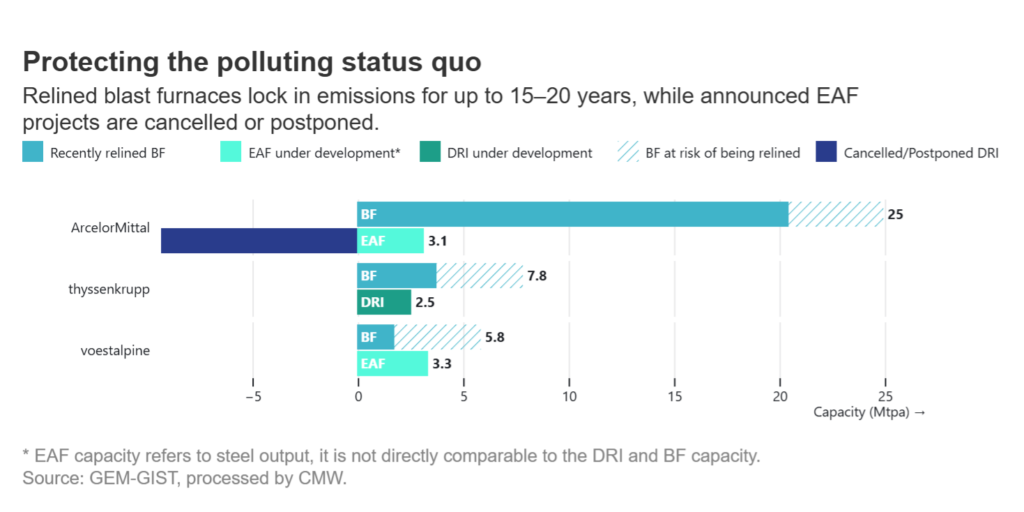

The polluting status quo

Evidence is emerging that the three major European steelmakers – Arcelormittal, thyssenkrupp and voestalpine – are more interested in protecting the polluting status quo, rather than investing in safe and reliable green steel infrastructure.

Over the past six years, ArcelorMittal, thyssenkrupp and voestalpine have made decisions to extend the life of many of their coal-based blast furnaces: this process is called “relining” and involves replacing the worn-out refractory bricks lining their interior. These decisions have prolonged the operations of carbon-intensive assets and locked in emissions for potentially as many as 15 to 20 years after relining. Moreover, a few relining decisions are still pending, potentially prolonging the lifespan of even more highly polluting plants well into the 2040s.

| All data related to plants, including on the value of relining investments, is sourced from Global Energy Monitor – Global Iron and Steel Tracker (GEM-GIST), unless otherwise specified. |

An infamous worst performer: ArcelorMittal

The biggest steelmaker in Europe (and the largest recipient of free allocation among all companies operating under the EU ETS) operates 11 blast furnaces in the EU. Despite being the market leader, ArcelorMittal is by far less efficient than the other steel firms, both in terms of CO2 emissions and in terms of input usage.

Of the 11, nine blast furnaces have been relined in the past five years (two at the site in Ghent, one at Eisenhüttenstadt, two at Bremen, two at Dunkerque, one at Dąbrowa Górnicza, and one at Fos sur Mer). The cost of these relining investments is estimated at €0.8-1.2 billion. Additionally, ArcelorMittal could decide to reline the remaining two blast furnaces of its fleet in the coming years, at sites in Gijón and Fos sur Mer.

Keeping these coal-burning, air-pollution spewing and climate heating furnaces running wasn’t always on the books. The blast furnace in Ghent was planned to be retired by 2030 and replaced by a cleaner green hydrogen-based DRI plant. However, the plan to open this new plant has been cancelled, and as a consequence it is unclear whether it will be retired.

The Ghent plant is not an outlier, several of ArcelorMittal’s decarbonisation projects have been paused, delayed or cancelled: the Gijon hydrogen DRI, as well as the Dunkirk DRI plan and the DRI and EAF in Bremen and Eisenhüttenstadt. These projects are worth around €4 billion, including state subsidies.

ArcelorMittal routinely received allowances for free, in excess of their verified and recorded emissions under the EU ETS. Between 2021 and 2025, ArcelorMittal received around 200 million free allowances, worth a total monetary value of over €15.5 billion. In 2024, they received free allowances equivalent to 111% of their verified emissions. During the same timeframe, their commitment to decarbonisation investments valued around €0.69 billion (part of which is covered by state aid). This is significantly less than €0.8-1.2 billion they have pumped into keeping their dirty plants running.

Having committed substantial capital to extending the lifetime of their carbon-intensive assets, the company has a firmer financial interest than most polluters to continue evading the EU’s carbon price. Weakening the EU ETS – or preserving more generous free allocations – protects the profitability of these investments by lowering ETS compliance costs and weakening the incentive to transition towards green steel production.

So what do steelmakers want?

Since 2020, ArcelorMittal, thyssenkrupp and voestalpine have relined blast furnaces for a combined capacity of about 26 Mtpa (million tonnes per annum), and they have no retirement plan for 24 Mtpa of that. In addition, for five plants representing another 12.7 Mtpa, a relining decision could be taken by 2030 and 2035, delaying their green transition by up to two decades. The additional sites that could be relined represent higher production capacity than all potential green steel production plants under construction.

The operating emissions of all plants combined – those relined and those at risk of relining – could result in around 65 Mt of carbon dioxide emissions per year. That’s almost as much as the yearly emissions of Austria. Every euro wastefully spent in extending the lifetime of blast furnaces could lead, depending on the future carbon price, to between €2 and €5 of additional operational cost due to ETS compliance each year. Investing in relining therefore means betting against the ETS.

At the same time, these three companies have continued to benefit from substantial subsidies to protect them from feeling the force of carbon costs. Between 2021 and 2025 they received an estimated €25 billion worth of free ETS allowances (over €15 billion for ArcelorMittal, and about €6.7 billion for thyssenkrupp and €3.3 billion for voestalpine). That doesn’t even include compensation for electricity carbon costs (so called ETS indirect cost compensation), or public funding for decarbonisation projects. Preserving overly generous free allocation reduces the cost of operating coal-based blast furnaces, including those with recently extended or soon-to-be extended lifetimes.

These companies are pushing to weaken the EU ETS while investing heavily to extend the life of blast furnaces. After years of ETS freebies and public subsidies, these companies are trying to argue that a watered down ETS is crucial for their business viability, when in reality, they are locking themselves into decades of high carbon emissions.

EU policymakers should not fall for this trap: the ETS is essential for EU companies planning to invest in a cleaner industrial future. These committed companies firmly support the need to decrease greenhouse gas emissions and to start paying a carbon price: the future of clean steel depends (also) on the ETS. Some are already playing their part, it’s high time the biggest polluters did so too.