Fresh evidence published by the Science Based Targets initiative (SBTi) confirms the unsuitability of carbon offsetting to meet emissions targets, echoing the findings of a new Carbon Market Watch study that casts doubt over the fairness of financial flows in the voluntary carbon market (VCM).

Today, the Science Based Targets initiative (SBTi), the world’s leading validator of private sector voluntary climate targets, released two papers proposing an updated framework to set scope 3 emissions targets, and an analysis of current scientific evidence on the performance of carbon offsetting.

The results contradict the controversial decision taken by the SBTi’s Board of Trustees in April, which defied the organisation’s own governance procedures and sparked a wave of protest from staff, advisors and organisations, including Carbon Market Watch. Such analysis also echoes previous CMW commentary on the lack of quality of studies that claim to show that offsetting emissions leads to higher climate ambition.

SBTi staff vs board

The meta-analysis of carbon credit quality published by the SBTi today is unequivocal: the overwhelming majority of high-quality and peer-reviewed journal articles demonstrate that carbon credits do not represent the climate benefits that they are claimed to represent, and using these to offset emissions inside a company’s value chain could lead to a weakening of global climate action. This makes carbon offsetting unsuitable for meeting corporate climate targets.

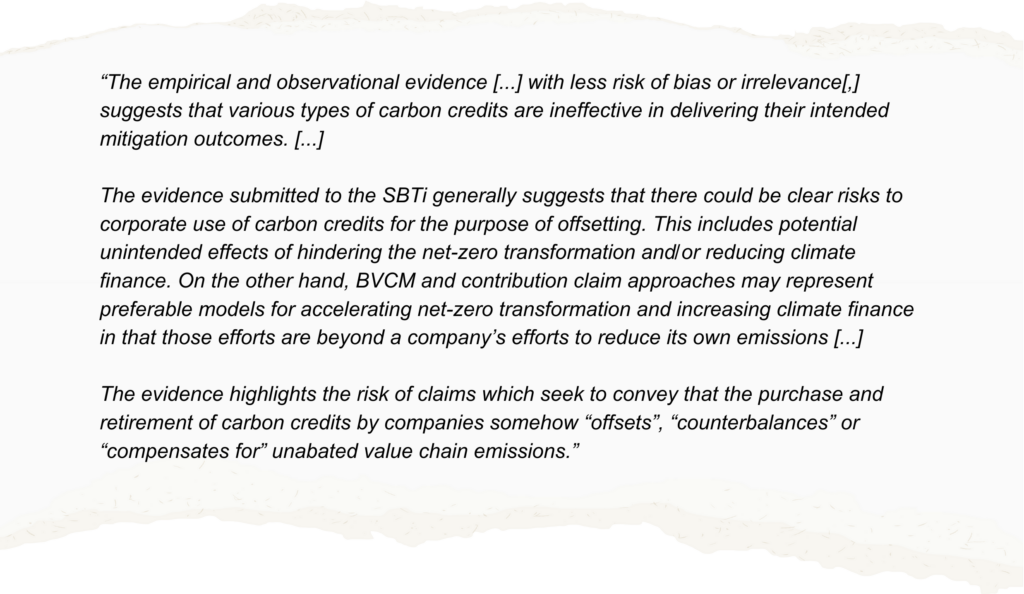

Quote from the SBTi paper:

This should inform SBTi as it deliberates over whether certain types of environmental attribute certificates (EACs), which include but are not limited to carbon credits, can play a role in achieving companies’ climate targets.

“This paper sets the record straight for SBTi, and is proof that SBTi staff are performing high-quality, unbiased work. It is a clear rebuttal of the Board’s April statement, where specific individuals tried to bulldoze through a proposal that did not have any internal support from SBTi staff or advisers,” explained Gilles Dufrasne, lead expert on global carbon markets at CMW. “The board should be guided by the staff, themselves guided by science, to take the right decisions about the role of EACs, not the other way around. Some certificates can play a positive role in corporate decarbonisation, but carbon offsetting is not one of them.”

North and south in the voluntary carbon market

Yesterday, CMW published our latest report ‘Due south’, which shows there is a large discrepancy between where carbon projects are located and the location where the majority of companies involved in these projects are based. From our sample of 39 African projects, 62% of the 101 companies involved were from rich (i.e. “developed”) countries, while no project was hosted in a developed country.

Less than 28% of companies involved in the African projects we looked at are actually based in an African country. The prevalence of companies from rich countries is also consistent across all VCM project participant roles: project developers, project owners, validation and verification bodies (VVBs), consultants, etc. Not only that, but these companies also carry out most of the roles in these projects.

*Based on a sample of 39 VCM projects across 39 African countries

“That the VCM is or could be channelling huge sums of money to the Global South is a baseless claim,” says Inigo Wyburd, policy expert on global carbon markets at CMW and author of the report. “Financial flows are obscured, benefit sharing arrangements are opaque, and we can now show that most companies engaged in the implementation of Global South projects are actually housed in the Global North.”

“The more we dig beneath the surface, the more doubts we have about whether the VCM truly contributes the money for mitigation actions in the countries that need the most support,” he continued. “It is high time for proponents of these mechanisms to show the evidence to back their dogmatic claims.”

This analysis builds on previous reports from CMW, which have exposed the total opacity of VCM intermediaries, as well as the lack of transparency and implementation of benefit sharing arrangements.