The International Maritime Organisation’s Net-Zero Framework is a necessary starting point but urgently needs greater ambition and binding revenue earmarking for decarbonisation and a just transition.

The shipping sector accounts for 3% of global greenhouse gas (GHG) emissions. This share could soar to 10% by 2050 at current growth rates.

Although the International Maritime Organisation (IMO) updated its climate strategy in 2023, the new targets remain far below what is needed to align with the Paris Agreement’s 1.5°C goal. Achieving that goal would require a 45% reduction in emissions by 2030, versus 20-30% in the IMO Strategy, which is, in itself, grossly overstated as our study will reveal. This means that the international shipping sector, under the stewardship of the IMO, is drifting way off course.

At its 83rd session in April 2025, the IMO’s Marine Environment Protection Committee (MEPC) was expected to agree on a set of mid-term measures to steer international shipping towards full decarbonisation, in line with the organisation’s updated greenhouse gas (GHG) strategy. Rather than adopting an effective carbon levy, the IMO settled on a weak compromise, which it optimistically called its ‘Net-Zero Framework’ (NZF): a hybrid approach combining a GHG fuel standard with a limited carbon pricing mechanism.

While a diplomatic success in troubled times and a starting point for action, the NZF falls far short of the ambition demanded by the escalating climate crisis. As civil society organisations warned right after the deal was sealed in April, the scheme doesn’t lead to enough emission reductions, does not price enough emissions, does not price those high enough, and does not generate enough revenue.

A forthcoming CMW study, led by Professor Michele Cincera from the Université Libre de Bruxelles (ULB), will provide data and in-depth analysis to highlight these critical gaps. The study will be published in November. This article provides a preview of the study’s main arguments and proposals before the IMO votes on the deal this week during the Marine Environment Protection Committee meeting in London (14-17 October).

While the NZF falls short of what is needed to tackle shipping emissions, it is essential that IMO member states vote in favour of the deal, work to strengthen it as soon as possible, and resist attempts to dilute its provisions further. Rejecting the framework and the chance of improving it would only be playing into the hands of the Trump administration and Big Oil, and delay the urgently needed decarbonisation of the shipping sector.

We call on IMO national delegations and relevant stakeholders to close the ambition gap as soon as possible through more ambitious GHG fuel intensity (GFI) trajectories, broader emissions coverage, and binding revenue earmarking for climate action and vulnerable states.

Speeding up action

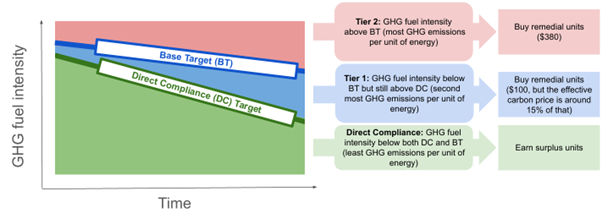

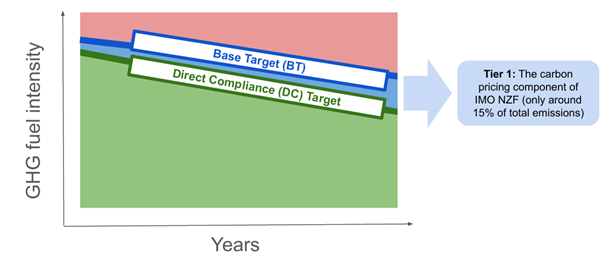

The IMO NZF scheme is based on a greenhouse gas (GHG) fuel standard for international shipping emissions. It is a command-and-control type of policy that operates through standards and penalties, comparable in its functioning to the EU’s FuelEU Regulation. Each year, it sets emissions targets through pre-determined GHG intensity reduction factors (also known as ‘Z factors’). As these emission reduction percentages become more ambitious over time, ships and fleets must lower their GHG fuel intensity (GFI), meaning the amount of GHG emitted per unit of energy used. For example, ships and fleets could lower their GHG fuel intensity with cleaner fuels.

Z factors are currently defined for each year from 2028, when the scheme is set to begin, to 2035 only. Two levels of ambition are provided: a less demanding ‘Base Target’ trajectory and a more ambitious ‘Direct Compliance’ curve. A Base Target level is also indicated for 2040. However, the IMO NZF does not refer to 2050 – the year around which international shipping must reach carbon neutrality under the IMO’s GHG Strategy.

Figure 1 outlines these trajectories and highlights the various compliance and non-compliance zones that fleets may fall into, depending on the amount of GHG emitted per unit of energy used.